Funding is the primary mechanism, which is used to tether the perpetual contract price to the spot price.

- Funding Calculation:

- Funding = Position Value * Funding Rate

- Funding Rate Calculation

-

Funding Rate = Clamp(MA(((Perpetual Buy order +Perpetual Sell order)/2-Spot Market Price)/Spot Market Price- Interest), a, b)

*Current Interest is 0

*a=-0.3%,b=0.3%

-

- Positive funding fee means that long positions pay short positions.

- Negative funding fee means that short positions pay long positions.

Funding occurs every 8 hours at 8:00 (GMT+8), 16:00 (GMT+8) and 00:00 (GMT+8), all traders who have open positions at one of these times, will either receive or pay a funding fee.

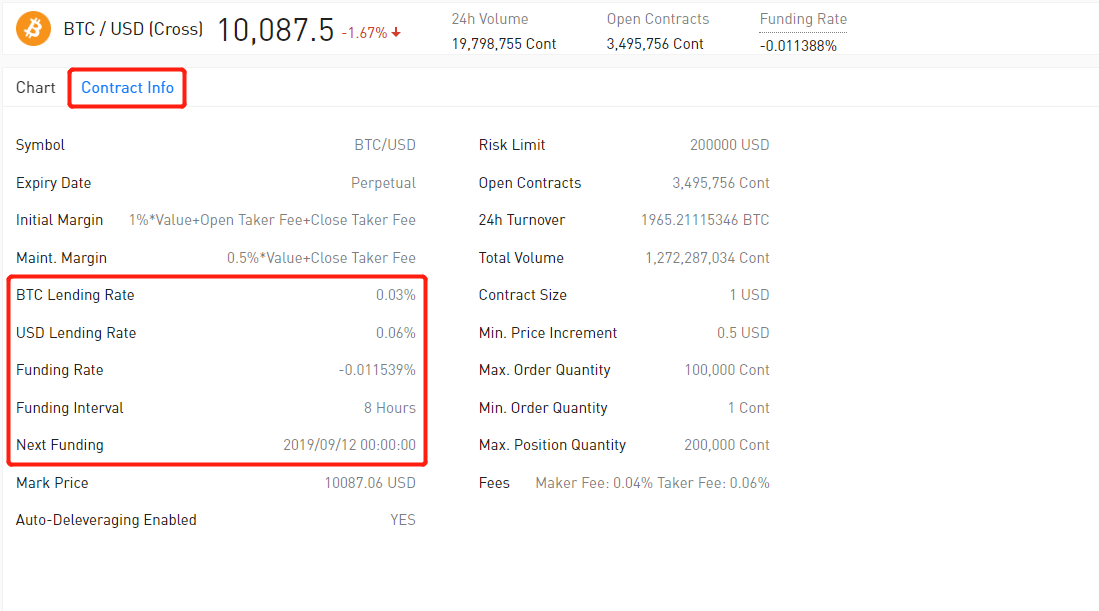

Contract Info are available by the Chart as below:

Example:

If John has a 1 BTC worth of Sell Short position and the Funding Rate is -0.006616%.

John then will pay funding to Buy Long side as a Sell Short side: 1 BTC*0.006745%=0.00006745 BTC.

Users with the Buy Long order will receive the Funding.

Comments

0 comments

Please sign in to leave a comment.